Scientific & Practical Journal

Editorial News

Dear readers! We are pleased to present you with the sixth issue of the journal for 2026, in which the theory and practice of logistics are explored in a variety of relevant areas. This issue is truly multifaceted, combining reflections on the essence of logistics processes with applied calculations and industry-specific cases.

Dear readers! This is the fifth issue of the LOGISTICS journal, dedicated to the current challenges of modern logistics.

Dear readers! We present you a new issue of the magazine dedicated to current logistics issues.

PHOTO OF THE WEEK

CITATIONS

|

|

|

|

|

|

|

|

|

|

|

|

All News of Logistics

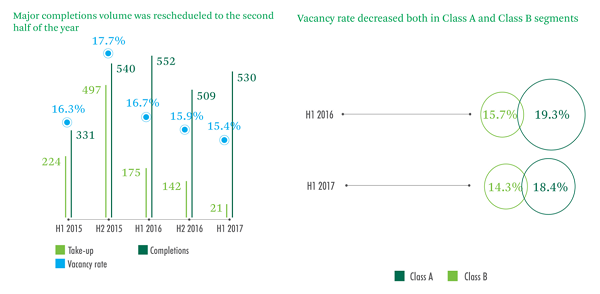

New office delivery volumes in Moscow are postponed to the second half of 2017

- Vacancy rate continues to decrease due to almost zero new completions volume –

CBRE, global real estate advisor, summarizes H1 2017 results of the Moscow Office market.

H1 2017 have experienced 530,400 sq m new leased and purchased for end-using purposes premises with just 4% lower compared to H1 2016. However, in H1 2016 take-up structure by 50% have been formed by sale transactions that were mostly non-market, while H1 2017 have experienced leasing transactions predominance (94%).

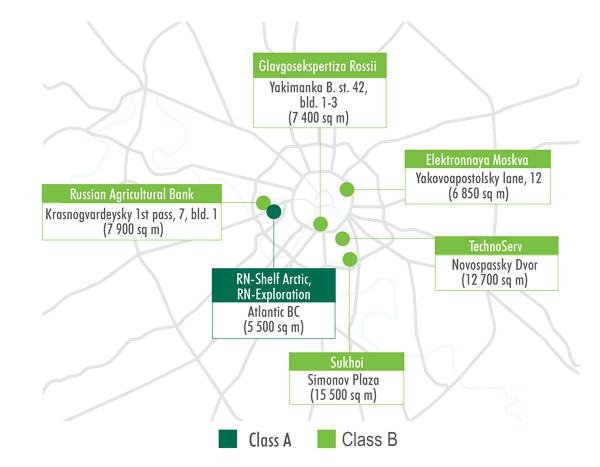

Largest deals in H1 2017

Source: CBRE, H1 2017

21,100 sq m of new office premises have been delivered in H1 2017 in Moscow (BC Dubrovka Plaza and new buildings in Bolshevik business centre), which is absolutely the lowest for over a last decade.

Office vacancy rate remains the downwards trend reaching 15.4% by the end of Q2 2017 which is 0.5 ppts lower compared to the 2016 year end and 1.3 ppts lower compared to H1 2016. For the last year vacancy rate decrease has been recorded both in Class A and B office markets: from 19.3% to 18.4% in Class A and from 15.7% to 14.3% in Class B.

Key Moscow Office market indicators

Source: CBRE, H1 2017

Elena Denisova, Senior Director, Head of Offices CBRE in Russia said:

"Vacancy rate decrease due to low new delivery volume and stabilized demand both in Class A and B has become the key trend in H1 2017. Meanwhile the lack of new buildings is deteriorating the collapse gradually formed on the market in a 2-3 years perspective, that will seriously affect medium and large-scale business. Current demand is still limited, whilst companies’ activity follows the recovery trend if compared to the preceding year. This activity conversion into the transactions in H2 or its failure will determine potential rental rates growth."

Address: 125581, Moscow, Leningradskiy avenue, 63,

floor 6, office 1

Phone: +7 (495) 788-16-96

Е-mail: sales@mg-agency.com

|

|

Total or partial reproduction of materials in any way

is allowed only with the written permission of the Publisher

Website developed by

alexeydoronin.com