научно-практический

журнал

Новости редакции

Уважаемые читатели! Представляем вам третий номер журнала, посвященный актуальным вопросам логистической отрасли.

Журнал «Логистика» принял участие в выставке TransRussia 2026. Работа на стенде стала очень продуктивной для нашей редакции и стала отличной возможностью напрямую пообщаться с целевой аудиторией – читателями, экспертами и партнерами. За три дня живого общения с аудиторией журнала позволили нам обсудить самые актуальные вопросы отрасли и получить ценные предложения для будущих номеров.

Уважаемые читатели! Представляем вашему вниманию второй выпуск журнала, посвященный актуальным вопросам логистической отрасли.

Статья недели:

ФОТО НЕДЕЛИ

ЦИТАТЫ

|

|

|

|

|

|

|

|

|

|

|

|

|

|

События в российской логистике

Q1 2020 investment volumes exceeded expectations

Investors’ activity will decline next half-year and the recovery of the market will start in 2021

Russia’s real estate investment volumes reached USD862m in Q1 2020, down 13% YoY from USD988m in Q1 2019. This is a fairly small reduction in Q1 investments YoY, although it is observed for the first time after the continuous positive dynamics of 2019.

«Real estate investments depend on predictable fundamental macroeconomic indicators, so the current situation has added a lot of uncertainty. The new reality, which is a deep shock for the Russian real estate market, has existed for three weeks only, so it is too early to predict the long-term impact. The lack of ability to forecast income from real estate portfolios for the next two-three months will stop most investment transactions. After the lifting of restrictive measures, we can expect the appearance of distressed assets, but their realisation will continue until at least 2021, – comments Vladislav Fadeev, Head of Research, JLL Russia & CIS. – Due to a halt in investment demand, only deferred transactions initiated in late 2019 or early 2020 will be closed in the next six months where they are economically feasible with a clear understanding of financing from the banking sector. The largest banks, primarily state-owned ones, should develop clear rules for debt restructuring for borrowers in the real estate sector in order to maintain continuing operations and to avoid unnecessary complications. The measures of Government and well-structured soft policies of banks towards borrowers in commercial real estate will potentially prevent mass bankruptcy».

Based on JLL's international experience, investment activity in the retail and hotel sectors will be most seriously affected so we do not expect any deals in the coming year, despite the recent stabilisation of the situation in Asian countries. At the same time, office and warehouse assets will be able to retain most of the revenue and remain attractive to investors.

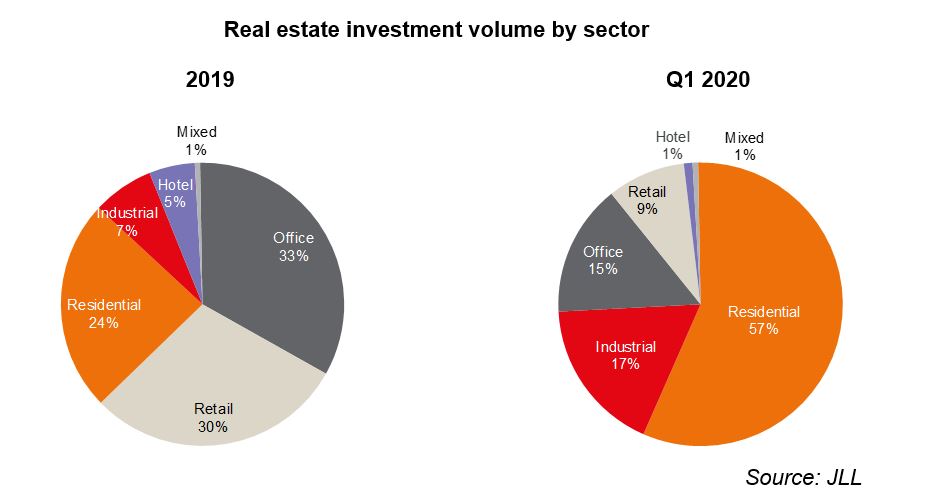

In Q1 2020, investors remained interested in land plots for residential projects, the share of investments in the residential sector was 57% of the total volume. The largest Q1 2020 deal was the purchase of two sites for residential development in Moscow by Capital Group.

The industrial sector followed with 17% of the total volume compared to 7% in 2019. Large deals were closed with Moscow and St. Petersburg assets. Due to the increase of demand from logistics and online retailers for warehouses investors’ attention to the industrial segment will grow this year.

The office sector completed the top-3 (15%) in the first quarter whereas it was the popular segment in the previous year.

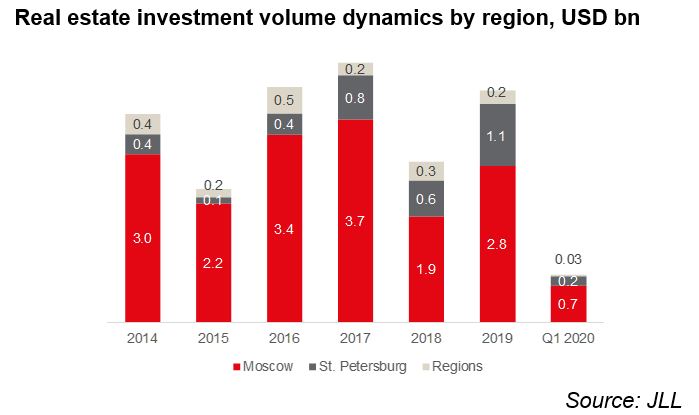

Due to the high demand from large investors for residential development sites, Moscow's share in the country's investment volume increased to 77% from 67% in 2019, while the share of St. Petersburg declined to 20% compared to 27% in 2019. The decrease of the Northern capital’s share in the volume of transactions was due to the unsusally high volume of the previous year, mostly driven by the purchase of large retail assets. The share of deals with regional assets (outside of Moscow and St. Petersburg) in the first three months of 2020 amounted to 3%.

The share of foreign capital in Q1 2020 investment volume reached 10% compared to 26% in 2019 reflecting a global trend of decreasing foreign investment in the world. The figure may continue to decline in H1 2020 due to absence of expected large transactions involving foreign players now.

Natalia Tischendorf, member of Board of Directors and Head of Capital Markets, JLL, Russia & CIS comments: «During the next few months owners and investors will be busy with their portfolios: stabilizing the rental flow, restructuring bank debts and optimizing staff, so we expect renewed interest in the investment market towards the end of 2020. Local players will return first due to their better understanding of the Russian market and readiness for more risky transactions. In addition, in 2020 we expect further increases in capitalization rates against the backdrop of increased macroeconomic uncertainty».

As benchmarks for the market now JLL analysts consider Moscow prime yields between 8.5-10.0% for offices and shopping centres and 11.0-12.0% for warehouses; St. Petersburg prime yields at 9.0-11.0% for offices and shopping centres and 11.0-12.5% for warehouses.

Адрес редакции: 125167, г. Москва,

Ленинградский пр-т, д. 39, стр. 14,

БЦ "Горбачев Фонд", этаж 5, офис 500В.

Тел.: +7 (495) 788-16-96, +7 (495) 945-38-20

Е-mail: info@mg-agency.com

|

Полное или частичное воспроизведение или размножение каким-либо

способом материалов допускается только с письменного

разрешения Издателя. разработка сайта

alexeydoronin.com