Scientific & Practical Journal

Editorial News

Dear readers! We are pleased to present you with the sixth issue of the journal for 2026, in which the theory and practice of logistics are explored in a variety of relevant areas. This issue is truly multifaceted, combining reflections on the essence of logistics processes with applied calculations and industry-specific cases.

Dear readers! This is the fifth issue of the LOGISTICS journal, dedicated to the current challenges of modern logistics.

Dear readers! We present you a new issue of the magazine dedicated to current logistics issues.

PHOTO OF THE WEEK

CITATIONS

|

|

|

|

|

|

|

|

|

|

|

|

All News of Logistics

Moscow Region Warehouses Register the Most Significant Decline in Vacancy in Six Years

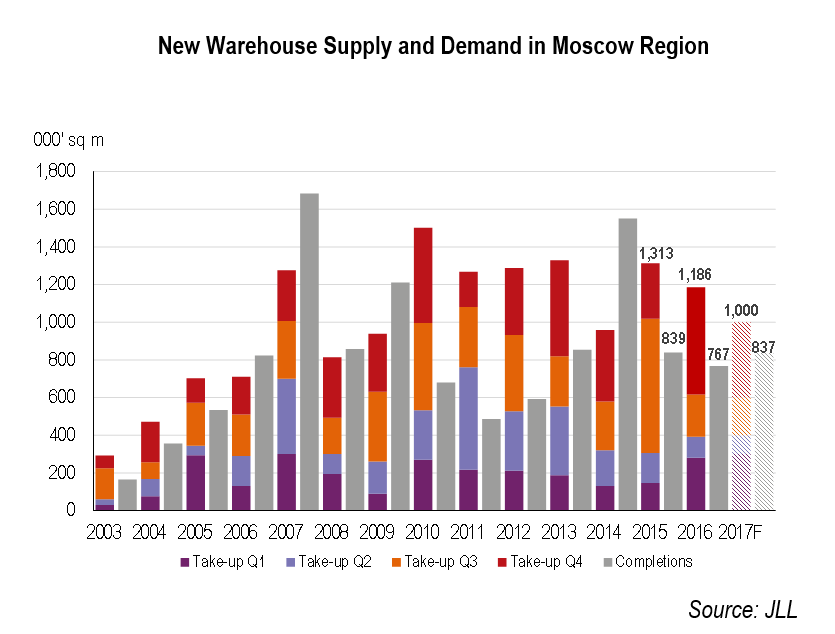

According to JLL estimates, the volume of new supply of warehouse space in Moscow Region in Q4 2016 has reached 570,000 sq m, the highest quarterly level in market history. The annual volume of new lease and sale transactions was 1.2m sq m, slightly below the 2015 level (1.3m sq m).

“The same volume of deals were transacted in Q4 2016 as in the first nine months,” - Viacheslav Kholopov, Regional Director, Head of Warehouse and Industrial Department, JLL, Russia & CIS, comments. – “Stabilization of the economy, absence of significant currency fluctuations and global political stability encouraged some companies to be more proactive in their plans. We expect tenants to remain active this year as well. Several negotiations are ongoing, with activity supported by the expiration of some short term agreements (2-3 years) signed during the ‘crisis period’ of 2014-2015 and long-term agreements. We expect the overall take-up in 2017 to roughly match last year’s level, at 1-1.1m sq m.”

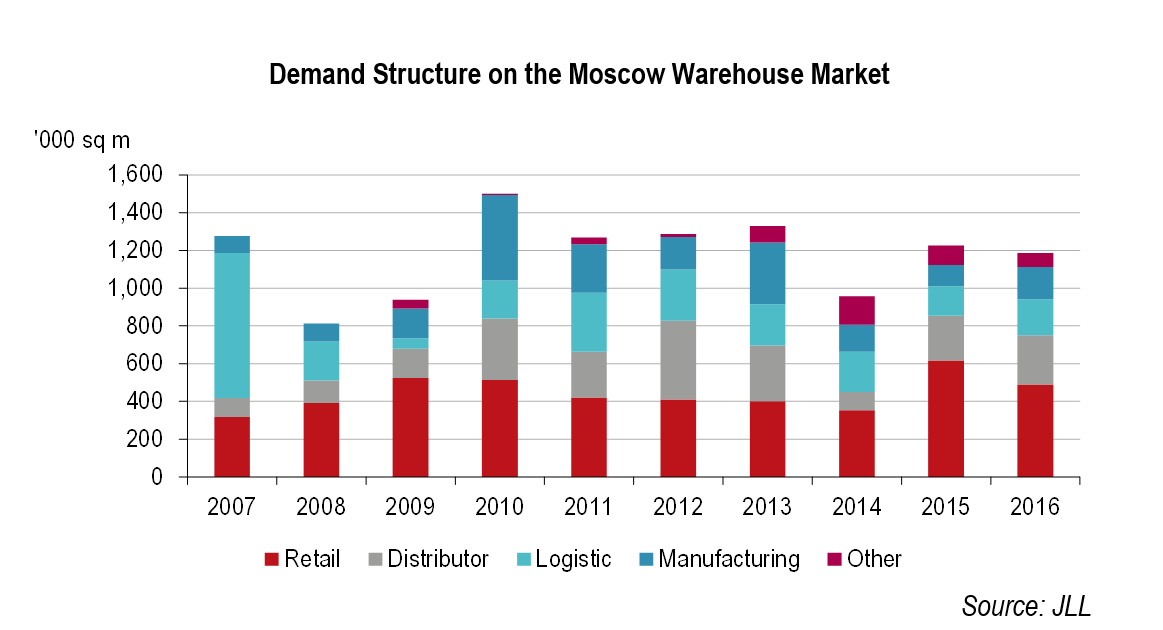

In 2016, retailers and distributors were the main demand drivers, accounting for 41% and 22% of all deals respectively. The share of retail operators declined slightly from that in 2015 (50%), whereas the share of manufacturing companies began to recover after a sharp drop last year – to 15% vs. 9% in 2015.

“The change of the overall political situation together with the adjustment of the business to the new economic situation resulted in the return of several players to the idea of relocation of manufacturing to Russia”, - Viacheslav Kholopov notes. – “In our view, 2017 will likely mark a beginning of a whole range of significant projects in Russia’s manufacturing sector, which will have a positive impact on the warehouse market.”

Against the pickup in demand, the volume of completions continued to decline in Q4 2016, by 11% compared to Q4 2015, to 143,000 sq m. The overall annual supply reached 770,000 sq m in 2016, 10% below the 2015 level. This decline was expected in the current conditions of high vacancy.

Among the largest warehouse completions delivered in Q4 2016, there are new premises in industrial parks PNK- Northern Sheremetievo, PNK-Valischevo (total area 165,000 sq m), South Gate (BTS for Leroy Merlin with the total area of 100,000 sq m), in Logopark Sever – 2 (85,000 sq m, BTS for O’key and Stolichnye Postavki); new logistic complex Vnukovo Logistic (50,000 sq m).

“The construction activity in the sector continues to slow, and last year’s completions have been twice lower the level in 2014 (1.55m sq m).” – Viacheslav Kholopov says. – “Currently there are over 800,000 sq m under construction which could be delivered this year.”

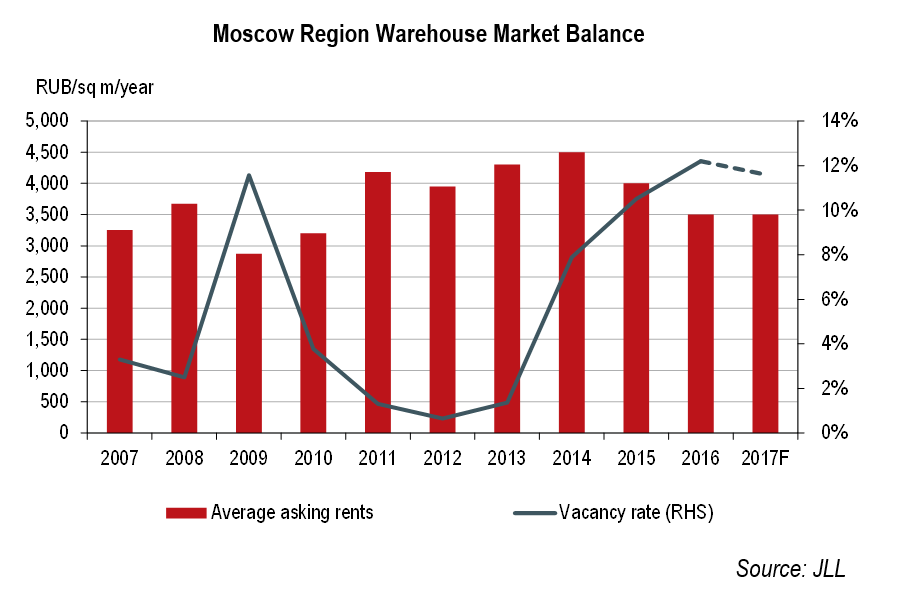

The record high take-up volume has led to the most significant decrease in the vacancy rate in the last six years, from 13.6% as of the end of Q3 to 12.2%, or 1.6m sq m in absolute terms. However, this still exceeds the rate at the end of 2015 (10.5%).

“Some deals last year (about 300,000 sq m) were signed as BTS schemes. Most of these will be constructed in 2017-2018. Note that this activity did not have any impact on the current level of vacant space,” - Viacheslav Kholopov highlights. – “Despite the significant volume of available space on the Moscow warehouse market, some companies prefer to wait for deliveries of new buildings for their projects. That is the sign for the market that the quality of the space is crucial for customers. Moreover, existing premises cannot be successfully adapted for the needs of every tenant.”

According to JLL analysts, if this year’s take up matches that of 2016, the vacancy rate will decline to 11.6-12% by the end of 2017.

The average level of asking rents for Class A space remained unchanged at RUB3,500-4,000 sq m per year (triple net). The competition between the buildings with high vacant space puts pressure on the developers to offer low rents. At the same time, growing construction costs and complexity of new project realization will put pressure on the upper level of the price range. According to JLL experts, rents may start rising in the beginning of the 2018.

Address: 125581, Moscow, Leningradskiy avenue, 63,

floor 6, office 1

Phone: +7 (495) 788-16-96

Е-mail: sales@mg-agency.com

|

|

Total or partial reproduction of materials in any way

is allowed only with the written permission of the Publisher

Website developed by

alexeydoronin.com